We’re not “stay out of debt” and “pay cash only” fanatics. It’s just that there can be good reasons for paying with cash instead of getting a loan, and we’ve had those good reasons. Yet when we have paid for our cars with cash, both times have been horrible and draining experiences. Lately, we have been trying to buy a cheaper home with cash, and that also has been an exceedingly stressful experience. “Cash is King,” right? So what’s the problem?

As far as I can tell, those buyers with lots of cash and the know-how to flaunt it, don’t have the same problems. When we were trying to purchase a condo in Orange County, California, a few years back, we could never do it because – as our agent told us – too many Chinese investors were here buying things up quickly with cash. In very short order, real estate prices rose and we were shut out of the market. (Why our own governments allows this . . . well, they allow it for the obvious reason that they prefer the influx of money over the the interests of its citizens and communities.)

This is what happened to us when we bought cars with cash. We didn’t buy either one from an owner, and I’m pretty sure buying from an owner would be much easier with cash. Anyway, we bought a used car from a dealership. It took FOREVER. They did a credit check, even though we weren’t paying with credit, and I believe they did a type of check that can be detrimental to one’s credit (I found out later). In any case, we ended up leaving with the car, having paid for it with a personal check. I thought they’d have one of those electronic check scanners and it would all be no problem; I was very wrong. Based on our experience, perhaps a call to the dealer ahead of time–asking what you can do to make the whole transaction easier and less time-consuming–might be helpful if you want to pay with cash.

The second car we purchased with cash was a new Kia Soul. That experience was even worse. It was UNBELIEVABLE. It was Valentine’s Day and we were there for 5-6 hours. I’m not kidding. We weren’t paying with a personal check, either, but told them we wanted the total so we could go get a cashier’s check just down the street from our credit union. The dealer was so ridiculous, having our salesman drive us to the CU and back; and this was only after we were walking out because it was getting to be so late in the day. What the what, right? We weren’t driving off with their property before paying for it, so I have no idea what their issues were. Our salesman wasn’t happy about it all, either, since it WAS Valentine’s Day and he wasn’t even originally scheduled to work . . . Since we were getting the better “online” price, he probably made a smaller than normal commission, too. But geez, KIA, don’t treat your customers like criminals!

So now we come to buying a home. Where we live now, we can’t buy a home, even with a large down-payment. The cost of living here is simply ridiculous for worker types, and that is one reason why we’re moving. Where we are moving to, the cost of living is far better and we can buy a “bottom-of-the-barrel” home with the amount we’d use for a down payment here. One reason we want to do it this way is that we don’t think we’d qualify for a mortgage when we have two months or more when we’d have to pay both a mortgage and rent. [1]

Also, with our health conditions, we’d rather have a cheaper home paid for in case one or both of us ends up on medical leave and we simply don’t have enough monthly income to pay a mortgage and everything else. However, we ARE planning on getting a home equity loan, if need be, to make repairs and improvements on the home after we move in. A home equity line of credit is the best deal at a local credit union, as far as I can tell, and the payments wouldn’t be bad at all. That way, too, we can update the home and make it more to our liking, instead of paying for a more expensive home that we would like to change some but can’t due to the already existing debt.

Ok, so what problems did we run into trying to buy a home with cash? Well, the problems are coupled with our wanting to move cross-country, so I don’t know if they’d be the same otherwise. This is all about relocating and not being able to get the help you need to do it. I thought cash would be easier in this regard, but now I think that having a pre-approved loan would be easier. With a pre-approved loan, the agents and sellers are probably going to feel more assured about who you are and all that. So that being said, we were trying to move to Grand Rapids, Michigan, but we literally couldn’t find an agent to help us. This made me realize that the laws and regulations regarding the buying and selling of homes need to change. You shouldn’t be barred from moving, relocating, because a private person–an agent and/or broker–won’t do their jobs. Can you imagine if you needed heart surgery and all the local surgeons said “Meh, he can go somewhere else”?

As far as I can tell, it would be less time consuming for an agent to help us than it would a local person. I can’t speak for everyone, but we would make an effort to whittle the choices down so the agent would only have a minimum of places to go to and visit for us (providing photos, insight, etc.). If the agent finds out what we want, s/he should be able to make a short list of available places ahead of time, anyway. But, I was told by agents that they simply didn’t want to deal with us in our situation at all. Period.

One broker even said he’d lose money on selling us a cheap home. [2] Since agents and brokers do a lot of work for FREE in the end–because a client doesn’t buy something with them and so there’s no commission at all for the time spent on that client–I don’t know how the agent could lose money when he made a commission. Even with that consideration, is it ethical to not help someone purchase a lower priced home, when agents are the gate-way to the seller? I’ve read a number of articles now that indicate that sellers often aren’t told of all the offers there are for their property. For an agent to not inform a seller of an offer is unethical and can have serious repercussions for the agent, yet it happens. So the attitude is already there, at least with some agents, to ignore buyers and their offers.

In the city we are now planning to move to (which I won’t disclose here), we had the same problem. But, we finally did get someone to help us (I think because it’s more of a buyer’s market there); still, it wasn’t at all the same as being there. We lost track of the agent for a while . . . we’re not sure what was going on. Then the agent told us we had to use the listing agent on a certain property, which we’re doing, but the new agent said that it wasn’t necessary to only use him. Oi. It’s all pretty crazy and mysterious. I can add a positive note, however. Years ago, when we were looking at the magically disappearing condos, the agents that helped us seemed to be quite open to spending time with us. One of them didn’t seem to represent us well, but at least they didn’t slam the door in our faces.

So, be warned. Buying expensive items with cash can be more difficult, in the extreme, compared to buying with credit. The western world we live in is a world based on credit. Everything is credit, even your identity in many cases . . . unless you’re a rich foreign investor, apparently. Of course, as Christians our true selves are known by God. Our “treasure in heaven” we’re supposed to be working on has nothing to do with credit, and it only has to do with money insofar as how much of it we give away and otherwise use for God’s purposes. Are we all living like that? Do we truly mean it when we pray, “your will be done, on earth as it is in heaven” (Matthew 6:10)?

So, be warned. Buying expensive items with cash can be more difficult, in the extreme, compared to buying with credit. The western world we live in is a world based on credit. Everything is credit, even your identity in many cases . . . unless you’re a rich foreign investor, apparently. Of course, as Christians our true selves are known by God. Our “treasure in heaven” we’re supposed to be working on has nothing to do with credit, and it only has to do with money insofar as how much of it we give away and otherwise use for God’s purposes. Are we all living like that? Do we truly mean it when we pray, “your will be done, on earth as it is in heaven” (Matthew 6:10)?

Notes

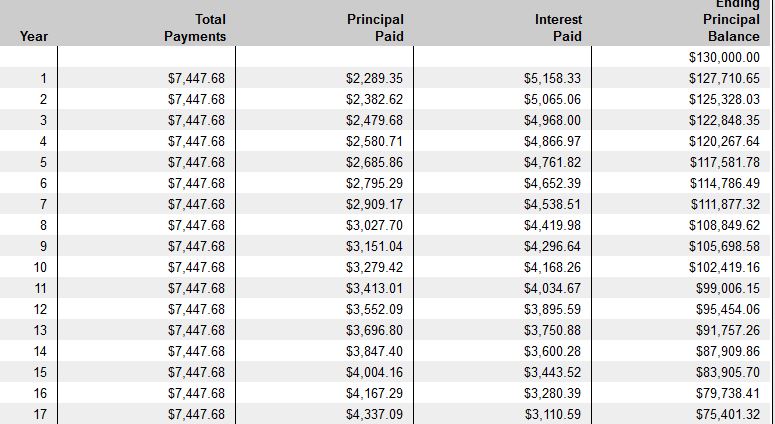

1. Besides that, if you don’t know already, when you get a mortgage you pay most of the interest on the loan at the beginning. Besides the amount of interest you end up paying being usury, if you’re not sure you’re going to be staying in the home for a long time, you’re wasting your money with a mortgage. For example, for a mortgage loan of $100,000 at 3.92% interest, with a 30 year term, you will pay an additional $70,213 in interest. So you end up paying over 70% more for the home, or at least 70% more on the portion of borrowed funds for the home. In the example below, you can see – if the print isn’t too small – how much goes toward principal and interest every year for the first 17 years of a 30 year mortgage. It isn’t until year 14 that more than half of your payment is going toward the actual loan and not interest!

2. The agent also said he simply wouldn’t help buy a home that was so cheap. It had to be a certain level of . . . what, livability? I think not. There often ARE problems with cheap homes, but some aren’t bad that we looked at. Some had even been totally refurbished and looked fine. I doubt if an investor would buy a fixer-upper that would be impossible or difficult to sell after putting all the labor and materials into it. This simply doesn’t make any business sense.